Date of publication: 20/04/2026

Our initial report on Auking Mining can be read here: ASX: AKN – Auking Mining

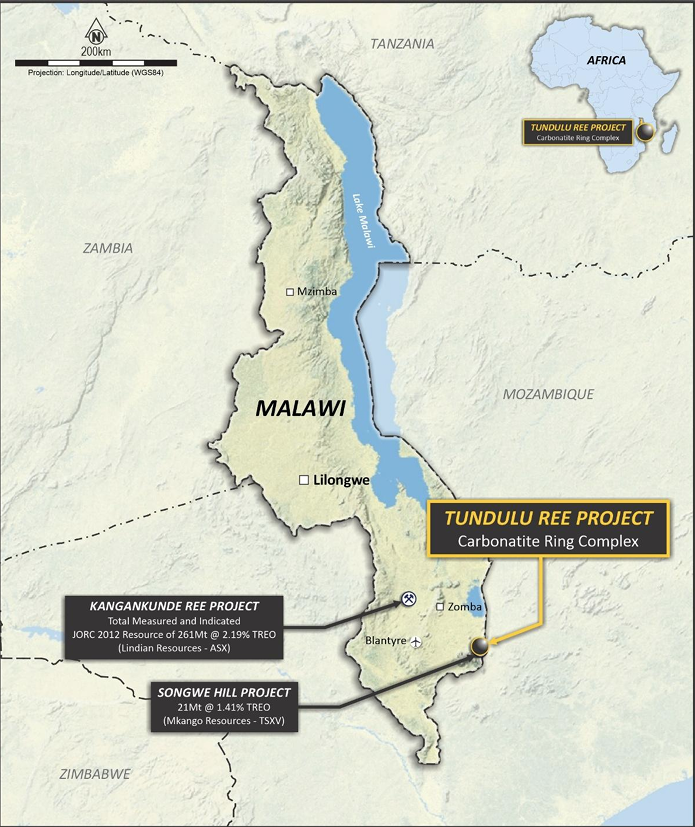

Tundulu Acquired: Large-scale underexplored Carbonatite Ring Complex

Geological analogue to Lindian Resources (A$1.5bn mcap) Kangankunde Carbonatite Rare Earths Deposit

Tundulu represents a compelling rare earth opportunity, with a proven rare-earth enriched carbonatite system in a proven geological neighbourhood.

The Tundulu project sits within the same Chilwa Alkaline Province as Lindian Resources (ASX: LIN) Kangankunde deposit, the same geological corridor that also hosts the Songwe deposit.

Key investment highlights

Same province as a A$1.5B project

Proven geological address

Tundulu sits within the Chilwa Alkaline Province alongside Kangankunde, sharing the same carbonatite suite, the same REE mineralogy, and the same hydrothermal formation processes.

Confirmed by independent JICA research

Geological analogue to Kangankunde

Japanese government research states Kangankunde carbonatites are “almost the same as those of Tundulu”, highlighting comparable mineral systems and strengthening the case for a similar-scale discovery.

Best intercept 30m @ 4.03% TREO from surface

Drilling confirms world-class grades

The 2014 programme across 55 holes returned intercepts including 97m at 1.35% TREO, 74m at 1.55% TREO, and 30m at 4.03% TREO from surface. Multiple holes ended in mineralisation; ore body open in multiple directions.

REE + phosphate + gallium

Three-commodity upside

Phosphate intercepts up to 30% P₂O₅ provide a second revenue stream. Confirmed gallium to 310 g/t Ga₂O₃ co-located with the REE target adds a third, in a market where China controls over 95% of global supply.

HREO averages 13% of TREO basket; Dy+Tb = 2.5%

Apatite-rich mineralisation

Tundulu hosts apatite-rich lithologies associated with rare earth enrichment, with hydrothermal upgrading identical to Kangankunde. REE-bearing apatite occurs alongside synchysite-(Ce) and bastnaesite with Dy and Tb at 2.5% of TREO.

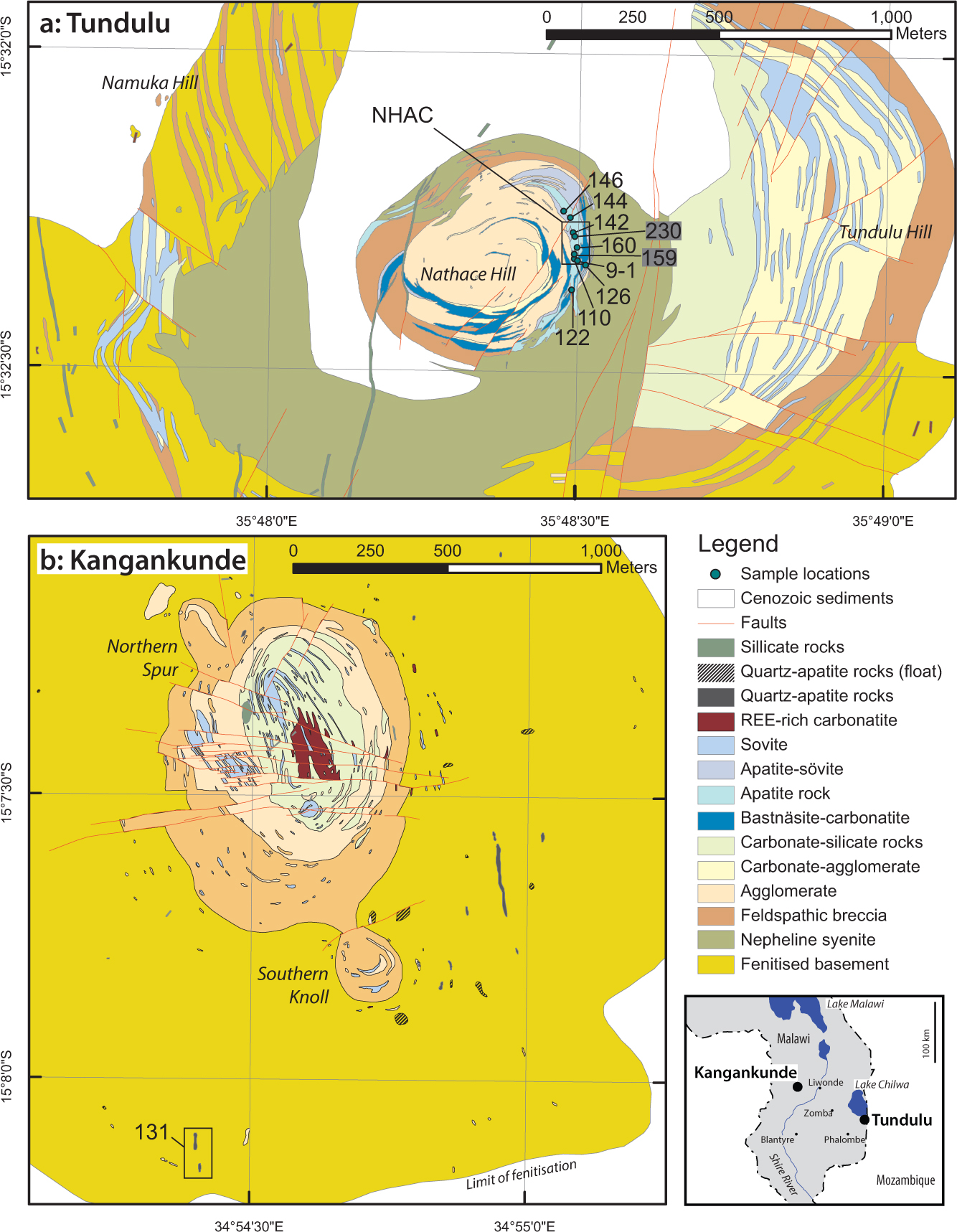

Six carbonatite hills, only one drilled

Ring complex offers substantial exploration upside

The 91.5 km² licence covers a 5 km carbonatite ring complex containing six documented carbonatite hills. All drilling to date has been confined to the eastern slope of Nathace Hill. The remaining five hills carry documented carbonatite outcrop and remain entirely undrilled.

Location

The Tundulu Rare Earths Project is located in the Phalombe District of southern Malawi, approximately 3 kilometres southeast of Lake Chilwa in the country’s Southern Region. The project sits within one of Africa’s most significant rare earths geological provinces, the Chilwa Alkaline Province, a late Jurassic to early Cretaceous suite of alkaline rocks and carbonatites that also hosts the nearby Kangankunde and Songwe Hill rare earths deposits.

The Tundulu Rare Earths Project is located in the Phalombe District of southern Malawi, approximately 3 kilometres southeast of Lake Chilwa in the country’s Southern Region. The project sits within one of Africa’s most significant rare earths geological provinces, the Chilwa Alkaline Province, a late Jurassic to early Cretaceous suite of alkaline rocks and carbonatites that also hosts the nearby Kangankunde and Songwe Hill rare earths deposits.

Malawi is a landlocked country in southeastern Africa bordered by Tanzania to the north, Mozambique to the east and south, and Zambia to the west. It is a stable, democratic jurisdiction with an established mining regulatory framework and a track record of attracting international resource investment. The country’s Mines and Minerals Act provides a clear and transparent licensing process, and the Malawian government has been actively supportive of critical minerals development as a pillar of national economic growth.

Tundulu boasts easy access to regional infrastructure. The commercial capital Blantyre, Malawi’s largest city with an international airport and established logistics services, lies approximately 90 kilometres to the west. The M1 highway, Malawi’s primary sealed arterial road connecting Blantyre to Lilongwe, runs through the broader region and provides the main freight corridor for the southern part of the country. Access to the project area is relatively straightforward, with the east side of the complex and Nathace Hill reachable via dirt road from the nearby village of Nambazo.

Mineralisation

Tundulu has been mapped, sampled and drilled across more than six decades. The foundational geological work was completed by M.S. Garson of the Geological Survey of Nyasaland in 1962, whose mapping of the three nested igneous centres remains the standard reference for the project today. The Geological Survey of Malawi drilled for phosphate at Nathace Hill through the 1970s and delineated a non-JORC historical resource of approximately 900,000 tonnes at 22% P₂O₅, with an additional estimated 1 million tonnes of apatite-bearing sovite grading greater than 10% P₂O₅.

The Japanese International Cooperation Agency (JICA) ran an exploration programme across the three major Chilwa Alkaline Province carbonatites in 1988. Tundulu received the largest allocation of the three sectors: 7.5 km² of geological survey area, 24 drill holes for 1,204.8 metres, and 243 ore samples, compared with 3.2 km² and 11 holes at Songwe and just 0.8 km² with no drilling at Kangankunde. The JICA programme included a standout intersection of 41 metres at 3.7% TREO from 8 metres at hole JMT-22. The JICA drilling was executed to a maximum depth of 50 metres due to rig limitations, and multiple holes terminated in high-grade mineralisation at that depth limit rather than at the base of the orebody.

A joint venture between Optichem and Mota-Engil added a further 55 holes for 7,002 metres of diamond and reverse circulation drilling at Nathace Hill in 2014, producing the bulk of the modern drill dataset. In 2016, Broom-Fendley et al. confirmed in peer-reviewed work published in American Mineralogist that Tundulu and Kangankunde in the Chilwa Alkaline Province, are each of particular economic interest for the extraction of materials considered critical.

The cumulative body of evidence describes a large, high-grade, multi-commodity critical minerals system centred on Nathace Hill, with substantial exploration upside across the five undrilled hills of the ring complex. Mineralisation takes two complementary forms: a rare earth carbonatite carrying high TREO grades with lower phosphate, and an apatite carbonatite carrying high phosphate grades with lower but still significant TREO. Lithological strip logs from the 2014 programme confirm a positive correlation between high-phosphate apatite and elevated heavy rare earth element content.

Uranium and thorium levels are low. A weighted average across all significant drilling intercepts returned 0.01235% thorium and 0.00187% uranium, well within levels considered non-NORM and comparing favourably to peers including Lynas Rare Earth’s Mount Weld deposit.

2014 Drilling Programme

The most substantive body of drill data was generated by a 55-hole diamond and reverse circulation programme completed in 2014, averaging 127 metres per hole with multiple holes terminating in mineralisation.

| Hole ID | From (m) | Interval (m) | TREO (%) | P₂O₅ (%) | Notes |

|---|---|---|---|---|---|

| JMT-17JICA 1988 | 36.2 | 13.9 | 4.11% | 0.02% | Highest-grade JICA intercept; grade increased with depth; hole terminated at 50.1m rig depth limit in mineralisation |

| JMT-22JICA 1988 | 8.7 | 41.1 | 3.68% | 0.03% | Longest continuous JICA intercept; near-surface start; hole terminated at 50.2m rig depth limit in mineralisation |

| TU014 | Surface | 30 | 4.03% | 0.35% | Second highest grade intercept on record at Tundulu |

| TU071 | 73 | 15 | 3.46% | 0.07% | High-grade zone within a broader 87m @ 1.19% TREO intercept from 5m |

| TU048 | 41 | 31 | 2.27% | 0.64% | High-grade REE carbonatite style |

| TU050 | Surface | 97 | 1.35% | 14.4% | From surface; highest P₂O₅ interceptBest P₂O₅ |

| TU042 | 30 | 100 | 1.09% | 12.6% | Elevated phosphate grade |

| HISTORICAL ROCK CHIP SAMPLES (JICA, 1988) : TO BE DRILL-TESTED | |||||

| 7Y386JICA 1988 | Surface rock chip | 6.41% | N/A | Nathace Hill; highest individual TREO surface sample in the JICA programme | |

| 7Y196JICA 1988 | Surface rock chip | 6.07% | 5.6% | Tundulu Hill eastern flank; highest grade sample from an undrilled hill within the ring complex | |

Source: DY6 Metals ASX announcements. 2014 programme: 55 holes for 7,000m of diamond and reverse circulation drilling at Nathace Hill. 1988 JICA programme: 27 holes executed to a maximum depth of 50m due to rig limitations. Rock chip samples from JICA 1988 geochemical survey of 85 samples across Nathace and Tundulu Hills; 25 samples returned greater than 1% TREO. TREO = Total Rare Earth Oxides. All drill intercepts are downhole widths; true widths not yet determined.

Trench TUTR10 Sampling (October 2024)

Sampling of 63 intervals across 83 metres returned up to 3.35% TREO and 27.5% P₂O₅. Average HREO content was 13% of the TREO basket, with dysprosium and terbium contributing 2.5%. The 120 kg composite returned 1.88% TREO and 9.07% P₂O₅. Undetectable mercury, lead and cadmium confirmed a clean deleterious profile.

Preliminary Metallurgical Testwork (2025)

Work at Auralia Metallurgy, Perth confirmed the viability of a dual product stream targeting a REE concentrate and a separate phosphoric acid grade phosphate concentrate.

Gallium Discovery (April 2025)

A review of 4,901 assay intervals from the 2014 programme identified significant gallium mineralisation, with 27.7% of all intervals returning greater than 40 g/t gallium oxide.

| Hole ID | From (m) | Interval (m) | Ga₂O₃ (g/t) | TREO (%) | Notes |

|---|---|---|---|---|---|

| TU043 | 72 | 74 | 93.26 | 1.56% | Highest grade interval; incl. 1m @ 310.46 g/t from 97m |

| TU014 | Surface | 30 | 94.63 | 4.03% | Co-incident with highest TREO intercept on record |

| RC hole | Surface | 53 | 72.79 | 1.02% | Incl. 12m @ 145.07 g/t from 25m |

| RC hole | 67 | 41 | 64.98 | 1.61% | Incl. 8m @ 178.94 g/t from 100m |

Source: DY6 Metals ASX announcement, April 2025. Gallium oxide (Ga₂O₃) grades from review of 4,901 assay intervals, 2014 drilling programme. 27.7% of all intervals returned greater than 40 g/t gallium oxide. Positive correlation confirmed between gallium oxide and TREO content across the dataset.

Summary of mineralisation indicators

Two independent drilling programmes spanning 26 years highlight the same interpretation: a large, high-grade, multi-commodity system that remains open at depth and along strike.

79 holes have been drilled at Nathace Hill across the JICA (1988) and Optichem/Mota-Engil (2014) campaigns, totalling over 8,200 metres.

Both programmes terminated multiple holes in mineralisation: the JICA rig hit its 50m depth limit inside 4.11% TREO at JMT-17, while four 2014 holes (TU073, TU087, TU094, TU110) ended in mineralised carbonatite at depths up to 179 metres.

✔ Three separate intercepts above 4% TREO across two independent programmes (JMT-17: 4.11%, TU073: 4.08%, TU014: 4.03%).

✔ Best surface sample: 6.4% TREO; 25 of 85 JICA rock chips exceeding 1% TREO.

✔ Sixteen significant drill intercepts, all exceeding 0.82% TREO, with continuous mineralised widths up to 125 metres.

✔ Grade increases with depth: JMT-17 progression from 0.65% at surface to 4.11% at hole bottom.

✔ Phosphate co-product up to 14.4% P₂O₅ across broad intervals, with undetectable mercury, lead and cadmium.

✔ Trench sampling up to 3.35% TREO and 27.5% P₂O₅; average HREO 13% of basket with Dy and Tb at 2.5%.

✔ 27.7% of 4,901 gallium assay intervals exceeding 40 g/t gallium oxide; peak grade 310 g/t Ga₂O₃.

✔ Non-NORM radioactivity: 0.00187% uranium and 0.01235% thorium weighted average.

✔ Dual product metallurgical pathway confirmed via preliminary testwork at Auralia Metallurgy, Perth.

✔ Only Nathace Hill drilled. Five of six carbonatite hills remain untested. The 91.5 km² licence remains largely unexplored.

Peer comparisons

Tundulu is the only true multi-centre carbonatite ring complex of the three principal rare earths deposits in the Chilwa Alkaline Province. Kangankunde and Songwe Hill are each single sub-kilometre carbonatite bodies. Tundulu is a five-kilometre ring complex containing six named carbonatite-bearing hills, bounded by a fenite aureole roughly twice the diameter of Kangankunde’s and more than three times that of Songwe Hill. The interactive comparison below shows all three deposits drawn to the same scale.

Tundulu vs. Kangankunde vs. Songwe Hill

Tundulu Project

- Nathace Hill: 500 to 600 m central vent (drilled, 41 m @ 3.7% TREO)

- Tundulu Hill: eastern hill, agglomerate & sövite dykes

- Makhanga Hill: western hill, unexplored carbonatite

- Namuka Hill: northern hill, unexplored

- Kamilala Hill: NE hill (Garson 1962)

- Chigwakwalu Hill: large southern hill, unexplored

- Three commodity streams: REE + phosphate + gallium

- 79 holes drilled, 8,200m; only eastern slope of Nathace tested

Songwe Hill

- JORC resource: 21 Mt M+I @ 1.41% TREO

- Reserve: 18.1 Mt @ 1.16% TREO

- DFS complete: NPV US$339M, IRR 24%

- 18-year mine life

- ~1.5 km fenite halo

Kangankunde

- JORC resource: 261 Mt @ 2.14% TREO

- Indicated: 61 Mt @ 2.43% TREO

- Reserve: 23.7 Mt @ 2.9% TREO

- Feasibility complete; entering development

- ~2.5 km fenite halo

Kangankunde (Lindian Resources, ASX: LIN)

Both the Tundulu and Kangankunde deposits formed during the same Late Jurassic to Early Cretaceous magmatic episode. They represent the second and third largest carbonatites in the Chilwa Alkaline Province. The same late-stage hydrothermal mineralising mechanism that concentrated rare earths at Kangankunde also operated at Tundulu, as documented by Broom-Fendley et al. (2016) in the American Mineralogist.

| Factor | Kangankunde (ASX: LIN) | Tundulu (ASX: AKN) |

|---|---|---|

| Geological maturity | Fully drilled; JORC resource and reserve defined; feasibility study complete | Exploration stage; ~60% of licence undrilled; no JORC resource estimate |

| Grade consistency | Exceptional; 2.5–3.5% TREO from surface to EOH across virtually every hole | Variable; high-grade zones to 4.03% TREO; apatite carbonatite zones carry phosphate co-product |

| REE basket | LREE dominant; NdPr ~20% of TREO | HREO-enriched; Dy+Tb = 2.5% of TREO; targets higher-value magnet metal market |

| Phosphate co-product | Minor; not included in feasibility study | Major; up to 30% P₂O₅; clean deleterious profile; comparable to Araxa and Sukulu |

| Gallium | Not identified | Confirmed; up to 310 g/t Ga₂O₃; co-located with REE target; China controls ~94% of global supply |

| Exploration upside | Largely defined; Phase 3 infill complete | Substantial; Tundulu Hill, Makhanga Hill, Namuka Hill, Kamilala Hill and Chigwakwalu hill undrilled. Nathace Hill only eastern slope drilled. |

| Market capitalisation | A$1.5 billion | A$28.6 million |

Sources: Lindian Resources and DY6 Metals ASX announcements; Broom-Fendley et al. (2016), American Mineralogist. Market capitalisations are approximate. Tundulu has no JORC-compliant mineral resource estimate. For informational purposes only; not financial advice.

Songwe Hill (Mkango Resources, TSX-V/AIM: MKA)

Songwe Hill shares the same REE-bearing minerals as Tundulu (synchysite and apatite) and the same hydrothermal formation mechanism. Mkango’s definitive feasibility study supports a post-tax NPV of US$339 million on just 21 Mt at 1.41% TREO.

Tundulu has not yet defined a resource. Yet on multiple geological metrics, Tundulu compares favourably or leads Songwe outright.

✔ Higher drill grades. Tundulu’s best intercepts of 4.03% TREO over 30 metres and 3.70% TREO over 41 metres exceed Songwe’s resource average of 1.41% TREO.

✔ Stronger HREO basket. Tundulu’s heavy rare earth content averages 13% of TREO with Dy and Tb at 2.5%, compared to Songwe’s approximately 7% HREO.

✔ Phosphate co-product. Songwe has none. Tundulu carries up to 30% P₂O₅ across multiple drill holes with a clean deleterious profile, potentially reducing effective capital requirements.

✔ Gallium. Songwe has none. Tundulu has confirmed gallium to 310 g/t Ga₂O₃, co-located with the REE target.

✔ Exploration upside. Songwe’s resource is substantially defined. Tundulu has drilled only the eastern slope of Nathace Hill and has not drilled the other 5 carbonatite bearing hills.

Mkango is valued at approximately CAD $305 million. Auking Mining, with a geologically superior drill profile and its licence still largely untested, is valued at A$28.6 million.

Commodities outlook

Rare earths

NdPr, dysprosium & terbium outlook

NdPr price gain YTD 2026

+136%

~$53/kg Jan 2026 to $124.87/kg

Permanent magnet CAGR to 2030

8.5%

Adamas Intelligence forecast

China share of supply chain

~90%

At separation and magnet stages

REE market size by 2035

US$12.6B

From US$7.2B in 2025; 6.5% CAGR

The structural demand case for rare earths has never been stronger, and supply has never been more politically contested. An average 100 kilowatt electric vehicle traction motor contains roughly 5 kilograms of neodymium-praseodymium and about 1 kilogram of dysprosium oxide. Direct-drive offshore wind turbines require approximately 600 kg of NdFeB magnets per megawatt of generating capacity. Both sectors are in rapid, government-mandated growth.

For heavy rare earths specifically, the supply picture is more acute. Dysprosium and terbium are scarcer outside China and are crucial for heat-tolerant magnets used in high-performance EV motors and defence systems. As of early 2026, no Western plant has achieved commercial processing of heavy rare earths. The result is that projects outside China, particularly in stable African jurisdictions with accessible, near-surface mineralisation, are increasingly valuable to Western governments and manufacturers seeking to de-risk critical supply chains.

- EVs: 5 kg NdPr and 1 kg dysprosium oxide per 100kW traction motor; global EV production has passed 20 million units annually

- Wind: ~600 kg of NdFeB magnets per MW for direct-drive offshore turbines; offshore wind capacity expanding rapidly

- Defence: 418 kg of rare earths in an F-35 fighter; 2.6 tonnes in a Type 51 destroyer; 4.6 tonnes in a Virginia-class submarine

- Supply: China controls 69% of mining and ~90% of downstream processing; no Western HREE processing at commercial scale as at early 2026

- Policy: EU Critical Raw Materials Act, US executive orders and IRA provisions all incentivise non-Chinese rare earth project development

Relevance to Tundulu

Tundulu's TREO basket averages 13% HREO, with dysprosium and terbium contributing 2.5%. This HREO enrichment positions a Tundulu concentrate in the highest-value segment of the rare earths market at a time when those specific elements face the most acute supply constraints and the steepest expected price increases.

Phosphate

Fertiliser market & food security outlook

Market size 2025

US$71.6B

Phosphate fertiliser market

Market size by 2040

US$176B

6.2% CAGR to 2040

DAP price gain 2025

+23%

World Bank fertiliser index

TSP price gain 2025

+43%

World Bank fertiliser index

Phosphate's investment case rests on two long-term pillars: a growing global population that cannot be fed without it, and a supply chain that is dangerously concentrated in a small number of countries. Global population is projected to reach 9.7 billion by 2050, adding roughly 2 billion mouths to feed on broadly the same amount of arable land. Phosphate cannot be substituted, manufactured synthetically, or recycled efficiently at scale. It is a finite, geographically concentrated resource with no alternative.

Regulatory tailwinds are strengthening demand for clean, low-contaminant phosphate sources. The European Union's cadmium limits are tightening access for phosphate producers whose rock carries elevated cadmium, including major North African and Middle Eastern suppliers. Low-cadmium, low-mercury phosphate from carbonatite sources commands a premium in European and premium Asian markets.

- Demand driver: Global food production must increase ~70% by 2050 to feed projected population; phosphate is irreplaceable in that equation

- Supply concentration: Morocco, China and Russia collectively control the majority of global phosphate reserves and exports

- China restrictions: Chinese export curbs in 2025 cut global availability and contributed to DAP prices rising 23% and TSP rising 43%

- EU cadmium limits: Regulatory tightening favours low-cadmium carbonatite phosphate sources with undetectable deleterious elements

- Battery demand: China redirecting phosphate to LFP battery production adds new internal competition for export tonnes

- New capacity: Maaden Phase 3 and Morocco expansions face multi-year timelines; tight market conditions expected to persist into 2026 and beyond

Relevance to Tundulu

Tundulu's apatite carbonatite zones carry up to 30% P₂O₅ across multiple drill holes, with undetectable mercury, lead and cadmium confirmed across all sampled phosphate-rich zones. This clean deleterious profile directly satisfies EU premium market requirements. A phosphate co-product from the same mining operation as the REE concentrate provides a second revenue stream that materially improves project economics and could reduce effective capital payback well below comparable single-commodity REE projects.

Gallium

Semiconductors, 5G & geopolitical supply risk

Price gain since Jan 2025

+141%

Spot ~$2,269/kg as at Mar 2026

Price gain since Jan 2020

+661%

From $298/kg to $2,269/kg

China share of production

>95%

Of global refined gallium output

Gallium market by 2030

US$7.97B

From US$2.87B in 2025; 22.7% CAGR

Gallium's price trajectory over the past two years has been one of the most dramatic in the critical minerals sector, and the structural reasons behind it are not going away. Gallium is not mined directly. It is recovered as a by-product of aluminium refining and zinc smelting, and more than 95% of global refined output comes from China. That production concentration, combined with rapidly accelerating demand from semiconductors, 5G infrastructure and electric vehicles, has created one of the most supply-inelastic critical minerals markets in the world.

Demand is growing structurally regardless of geopolitics. Gallium arsenide and gallium nitride semiconductors are essential for 5G base stations, radar systems, EV power electronics and satellite communications. Each 5G base station contains 8 to 12 specialised gallium arsenide integrated circuits. Gallium nitride power semiconductor adoption in electric vehicles grew from 5% of new EV models in 2020 to approximately 30 to 40% of new platforms by 2025 to 2026. The EU Critical Raw Materials Act names gallium as a strategic raw material and mandates that member states work toward reducing single-source import dependency.

- 5G: Each base station contains 8–12 specialised GaAs RF integrated circuits; approximately 2.3 million 5G base stations deployed globally as at 2025

- EVs: GaN power semiconductor adoption in new EV platforms grew from 5% (2020) to 30–40% (2025–2026); reduces switching losses by 40% vs silicon

- Defence: Gallium compounds used in radar, guided munitions and satellite communications; classified as strategically critical by US and EU

- Solar: CIGS thin-film photovoltaics use gallium; higher efficiency than conventional silicon panels in building-integrated applications

- Supply gap: Meaningful Western gallium production capacity not expected before late 2020s; Greece's Metlen facility targeting 50 tonnes/year by 2027

- Price floor: Security-of-supply pricing is structural; prices expected to remain well above pre-2023 levels even if Chinese exports resume fully

Relevance to Tundulu

The 2025 review of 4,901 assay intervals from Tundulu's 2014 drilling programme confirmed that 27.7% returned greater than 40 g/t gallium oxide, with a best intercept of 310 g/t Ga₂O₃. The gallium is co-located with the primary REE target with no separate drilling or infrastructure required. No exploration has been conducted on the deeper gallium potential at Tundulu. This is a third commodity stream in a market where China controls over 95% of supply, prices have risen 661% since 2020, and Western governments are actively funding any credible alternative source.

Sources: Adamas Intelligence; World Bank Commodity Markets Outlook; IDTechEx Rare Earth Magnets 2026–2036; Mordor Intelligence; Grand View Research; skillings.net; strategicmetalsinvest.com; DY6 Metals ASX announcements. Market data and price references as at April 2026. This content is for informational purposes only and does not constitute financial advice.

Summary

Tundulu is an early-stage critical minerals project with the geological foundations of something considerably larger.

3x 4%+

TREO intercepts

1 of 6

Hills drill-tested

3

Critical mineral streams

~52x

Peer valuation gap

Drilling confirms a large, high-grade system

Two independent programmes, 26 years apart, tell the same story

Three separate intercepts above 4% TREO across the 1988 JICA and 2014 Optichem/Mota-Engil programmes, with both campaigns terminating holes in mineralisation. The JICA rig hit its 50m depth limit inside 4.11% TREO at JMT-17, with grade increasing from 0.65% at surface to 4.11% at hole bottom. The 2014 programme confirmed mineralisation persists to at least 179 metres, with continuous intercepts up to 125 metres. All drilling has been confined to the eastern slope of Nathace Hill. The western face, southern approach, central peak, and the five remaining carbonatite hills are entirely untested.

Three-commodity upside in one deposit

Rare earths, phosphate and gallium from the same mining operation

Rare earths enriched in the highest-value heavy elements: dysprosium and terbium at 2.5% of the TREO basket, at a time when China's Announcement 18 export controls have driven prices to multi-year highs. A phosphate co-product with intercepts up to 14.4% P₂O₅ and undetectable mercury, lead and cadmium, directly satisfying EU premium market requirements. Gallium confirmed at grades up to 310 g/t Ga₂O₃, co-located with the REE target, in a market where China controls over 95% of global supply and prices have risen more than 600% since 2020.

Provincial context validates the potential

Same corridor as a A$1.5B project entering development phase

Kangankunde, in the same Chilwa Alkaline Province, is valued at approximately A$1.5 billion and entering development. Songwe Hill supports a post-tax NPV of US$339 million on just 21 Mt at 1.41% TREO. Tundulu's best drill grades exceed both peers' resource averages, its HREO basket is richer, and it carries two additional commodity streams that neither Kangankunde nor Songwe has. Independent Japanese government (JICA) research confirmed the carbonatites at Kangankunde and Tundulu are "almost the same" in character.

The larger prize lies beyond Nathace Hill

Five carbonatite hills undrilled, western and southern faces untested

All 79 drill holes across both programmes have been confined to the eastern slope of Nathace Hill. The western and southern faces of Nathace remain untested. REE mineralisation remains open in both directions and towards the central peak. Beyond Nathace, five carbonatite hills within the ring complex (Tundulu, Makhanga, Namuka, Kamilala and Chigwakwalu) carry documented carbonatite outcrop and have never been drilled. It is discovery.

Chilwa Alkaline Province: market capitalisation comparison

Same geological province. Same carbonatite suite. Same REE mineralogy. ~52x valuation gap.

The re-rate potential begins with resource definition at Nathace Hill, where drilling has so far been confined to the eastern slope. But the larger prize may lie beyond it. Five carbonatite hills within the ring complex have never been drilled, the western and southern faces of Nathace remain untested.

At Tundulu, the upside is not just resource definition. It is still discovery.