ASX: AKN

Our investment pick:

AuKing Mining

Low market cap, high-grade tin and uranium exposure

AuKing Mining has acquired a portfolio of prospective tin and silver assets in Tasmania that remain significantly under-explored and offer substantial discovery upside.

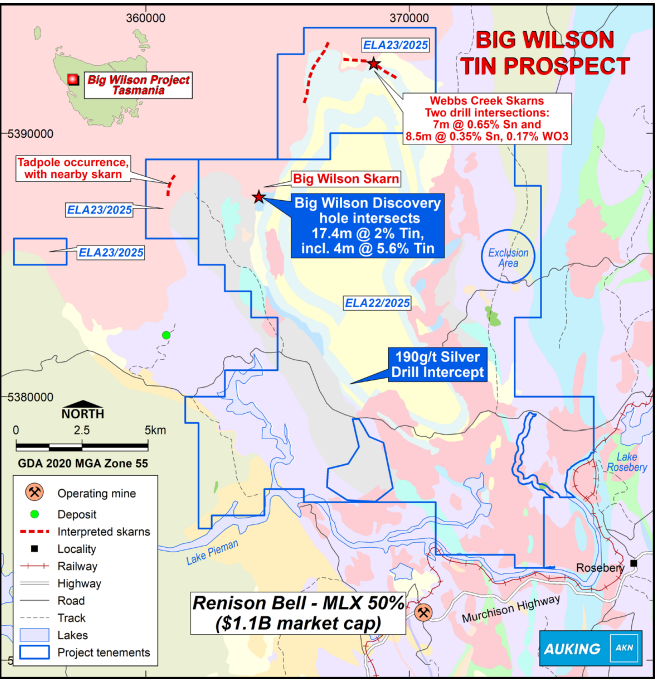

The Big Wilson tin prospect is a standout example. The prospect was identified from a high-grade tin discovery hole from an initial wide-spaced drilling program completed in 2012 by Venture Minerals. The standout discovery hole, BW001, returned an exceptional 35.4 metres at 1.0% Sn, including 17.4 metres at 2.0% Sn and a high-grade core of 4.0 metres at 5.6% Sn. These results highlight the potential of an underlying fertile tin system.

Following the initial 13-hole reconnaissance drilling program in 2012, no additional drilling or targeted exploration was undertaken to define the mineralised system or to evaluate the full extent of the 1.1 kilometre-long tin anomaly identified at Big Wilson. The project remains largely under-drilled, with significant scope to improve geological understanding and unlock value through systematic follow-up exploration.

Strategic entry into a proven tin district

AuKing Mining’s newly acquired exploration licence applications lie in a proven tin district of global significance on Tasmania’s West Coast. The tenements are immediately adjacent to the Renison Bell tin operation, which is Australia’s largest tin producer. Renison is operated by Bluestone Mines Tasmania Joint Venture Pty Ltd, a 50/50 partnership between Metals X Limited and Yunnan Tin Group, one of the world’s largest refined tin producers.

The Renison mine boasts a substantial tin inventory and robust production profile, with approximately 396,000 tonnes of contained tin at a grade of 0.93% Sn and 89,300 tonnes of contained copper at 0.21% Cu as previously reported.

Renison’s ongoing success, supported by consistent production and reserve life extensions, reflects both the size of the tin system and the strength of regional geology. The district also hosts other tin projects such as Stellar Resource’s Heemskirk Tin Project, which contains a significant high-grade tin mineral resource of 77,872 tonnes at over 1.04% Sn, reinforcing Tasmania’s West Coast as a tier one tin province.

This extraordinary tin endowment and well-established mining infrastructure enhances the prospectivity of the ground AuKing has secured. The licence areas, including the Big Wilson prospect, are positioned within the same structural corridors and granite-related mineral systems that have produced multiple commercial tin deposits and continue to attract exploration interest. The combination of proven regional mineralisation, world-class nearby resources and under-explored tenure offers a compelling platform for systematic exploration.

Big Wilson Tin Prospect

![]()

-

Hosts a confirmed high-grade tin discovery from historical drilling by Venture Minerals.

-

Discovery hole BW001 intersected 35.4 m at 1.0% Sn, including 17.4 m at 2.0% Sn and 4.0 m at 5.6% Sn, demonstrating a fertile tin system.

-

Mineralisation occurs as cassiterite in greisen and skarn, a proven style for economic tin deposits in Tasmania.

-

The discovery sits within a 1.1 km long tin-in-soil anomaly, indicating significant strike potential.

-

First pass reconnaissance drilling by Venture Minerals was extremely wide spaced and never followed up with systematic step-out or infill drilling, leaving the system effectively under-defined.

-

Represents a clear opportunity to delineate scale and continuity with modern exploration.

Merton Hill Prospect

![]()

-

Located in the southern portion of the licence area.

-

Historical workings and shallow drilling recorded tin, silver, lead, zinc and copper, indicating a polymetallic system.

-

Mineralisation is associated with favourable host rocks and structures analogous to other West Coast deposits.

-

Exploration to date has been limited and shallow, with no modern targeting or geophysical integration.

-

Offers potential for both tin-dominant mineralisation and silver-rich polymetallic zones.

Laurel Creek / Webb’s Creek Prospect

![]()

-

Historical drilling by Gold Fields Exploration Pty Ltd intersected tin and tungsten mineralisation, including skarn-hosted zones. The drilling consisted of a 5-hole shallow diamond program in 1983-1984.

-

Reported intersections include multi-metre tin intervals at grades consistent with economic skarn systems.

-

-

-

(WR1) 8.5m @ 0.35% Sn from 63m

-

(WR5) 7m @ 0.65% Sn from 66m

-

-

-

-

Skarn mineralisation in this district is spatially associated with Devonian granites, the same regional drivers that underpin Renison and other major deposits.

-

The area has not been systematically re-evaluated using modern geological models or geophysics.

-

Strong potential for tin-dominant or tin-tungsten mineralisation with further exploration.

Regional and Conceptual Targets

![]()

-

The tenements cover a large, contiguous land package in a proven tin belt adjacent to the Renison Tin operation.

-

Numerous untested soil and stream sediment anomalies remain within the licence area.

-

Structural corridors and granite contacts known to host tin mineralisation extend into the tenements but remain under-explored.

-

Provides a pipeline of early-stage targets capable of generating new discoveries, not just extending known systems.

Tin has surged 91.2% in the past twelve months

Tin supply fundamentals have been deteriorating due to a prolonged lack of exploration and discovery of new tin deposits. Tin prices have approached all-time highs in part because there has been minimal investment in the discovery of new deposits. The result is a scarcity of new supply to take up the slack from ageing mines and natural depletion.

Tin plays a central role in the electronics industry, with solder representing around 50 per cent of global demand, underpinning strong and growing consumption driven by the energy transition and accelerating digitalisation.

With tin markets estimated at only 350,000-380,000 tonnes of annual consumption, limited exploration means few new production sources are ready to replace or expand supply, amplifying price responses when existing supply is tight.

Indonesia is traditionally the world’s second-largest tin supplier (behind China), and regulatory actions there have had outsized effects on global markets.

The Indonesian government has cracked down on illegal tin mining operations, with enforcement actions targeting potentially thousands of unregulated sites. These operations historically accounted for a significant portion of exportable tin supply.

This regulatory intervention tightened supply and removed material volumes of concentrate from global export channels, contributing directly to rising base metal prices.

Indonesia’s export permitting system has also experienced seasonal delays and stricter compliance requirements, which have curtailed official export flows and slowed post-crackdown recovery.

Tin supply from other major producers such as Myanmar and the Democratic Republic of the Congo remains exposed to geopolitical and regulatory risk, constraining reliable mine production and exports.

China, Myanmar, Indonesia and the Congo (DRC) accounted for approximately 59.3% of total global Tin mine production in 2024.

Tin: Key Applications

| Application | Description |

|---|---|

| Electronics | Tin is the primary component in solder, which is used to join electronic components to circuit boards. Modern solders are typically tin-based alloys following the phase-out of lead. Every smartphone, computer, server, data centre, electric vehicle, solar inverter and piece of AI hardware relies on tin solder. There is no scalable substitute that matches tin’s low melting point, conductivity and reliability. |

| Tinplate for Packaging | Tin is used as a thin protective coating on steel to create tinplate, which prevents corrosion and contamination. Tinplate is critical for food safety, as tin is non-toxic and provides a stable barrier between steel and consumables. |

| Chemicals and Catalysts | Tin compounds are used as catalysts and stabilisers in chemical processes, including plastics and coatings. Tin-based catalysts enable efficient polymerisation and improve product durability, heat resistance and performance. |

Date: 03/02/26

Ticker: AKN

SOI (undiluted): 1,196,779,441

Share price: $0.013

Market cap (undiluted): $9.57m

Cash (approx): $1.5m

Percentages are indicative only. Country production figures and global totals are based on USGS estimates and rounding may result in totals not equalling 100%.

Mkuju Uranium Project, Tanzania

The Mkuju uranium project is located in southern Tanzania within a globally recognised uranium province. The Mkuju district is widely regarded as Tanzania’s most significant uranium region, hosting the country’s largest historical uranium discoveries and demonstrating clear geological endowment for large-scale sandstone-hosted uranium systems.

Mkuju sits adjacent to, and within the same geological setting as, the Nyota uranium deposits, which were previously advanced by Mantra Resources and collectively reported to contain more than 100 million pounds of U₃O₈ @ 422 ppm in historical resource estimates. These deposits attracted the acquisition of Mantra by a Rosatom subsidiary, underscoring the strategic importance and scale potential of the Mkuju uranium province.

Rosatom subsidiary acquires Mantra Resources for A$1.2bn

The uranium mineralisation style at Mkuju is sandstone-hosted, a globally proven deposit type that underpins major uranium operations in Kazakhstan, Namibia and Australia. This style is typically characterised by broad, laterally extensive mineralised zones, favourable metallurgy and potential for scalable development.

AuKing undertook first-pass exploration at the Mkuju project in 2023, comprising 56 auger drill holes to a maximum depth of 13 metres. In addition, 67 soil samples and 18 rock chip samples were collected for geochemical analysis.

Standout results from the campaign include:

Auger

- 1m @ 160ppm U (MKAU23_014)

- 3m @ 1273ppm U (MKAU23_020)

- 1m @ 130ppm U (MKAU23_035)

- 3m @ 250ppm U (MKAU23_045)

Soil Sampling

- 480ppm U (MKSS001)

- 510ppm U (MKSS006)

- 8,800ppm U (MKSS016)

- 170ppm U (MKSS042)

- 960ppm U (MKSS052)

- 410ppm U (MKSS053)

Rock Chip Sampling

- 2,250ppm U (MKRS011)

- 800ppm U (MKRS012)

Following first-pass exploration completed in 2023, the project remains undrilled, with AuKing Mining planning to commence drilling as funding allows.

Uranium Market Remains Buoyant

Uranium pricing has strengthened significantly in recent months as market fundamentals tighten. Benchmark spot prices have been trading above US$80-90 per pound U3O8, with industry models suggesting prices could approach or exceed US$100 per pound later in 2026 as demand continues to rise and supply remains constrained.

Uranium increased 40% over the past 12 months (2025-2026)

The market has shown renewed momentum as long-term contracting and utility purchasing increases, with many recent contracts executing at price floors often well above the traditional published spot levels. This reflects a shift in pricing dynamics where utilities are securing future supplies in an environment of tightening inventories and growing procurement urgency.

On the supply side, the industry has experienced years of underinvestment in new mining capacity, with only limited new production coming online. Major producers have generally maintained disciplined output, and secondary sources such as stockpiles and re-enrichment programmes are finite and cannot fully bridge the gap between rising consumption and available supply.

Demand for uranium is being driven by a global expansion of nuclear power capacity. Several countries are actively building or planning new reactors to provide reliable, low-carbon baseload electricity as part of broader climate and energy security policies. This growth in reactor fleets is expected to lift uranium requirements materially through the remainder of this decade and into the 2030s.

Additional factors supporting a bullish price outlook include increased institutional investment, heightened strategic stockpiling by utilities, and policy support in key markets. These are contributing to both near-term upward price pressure and stronger long-term contracting trends that underpin future demand.

Taken together, the uranium market outlook remains strong. Prices are elevated relative to the past decade, demand is structurally growing due to nuclear expansion, and supply responses are slow, creating a backdrop where higher sustained uranium pricing is a credible expectation as market participants adapt to shifting fundamentals.

Additionally, the United States and European Union have adopted policy initiatives that has further increased demand on Uranium.

In November 2025, the United States Geological Survey (USGS) reinstated uranium on its list of critical minerals, reversing its removal in 2022. In 2024, the Prohibiting Russian Uranium Imports Act was enacted, banning the import of enriched uranium from Russia, previously a major source of nuclear fuel for U.S. reactors.

Assays of exploration work undertaken by Manta Resources and Uranex NL on the Mkuju tenue now owned by AuKing Mining.

Koongie Park/Halls Creek, Copper/Zinc project

In February 2025, AuKing Mining and Cobalt Blue (ASX: COB) entered a joint-venture for the Halls Creek Project, also known as the Koongie Park Project, located in the highly mineralised Kimberley region of Western Australia. Under the joint-venture terms, Cobalt Blue can earn up to 75% interest for funding $2M in exploration and development expenditure over a 3 year period.

The project sits approximately 15 kilometres south-west of the Halls Creek township on the Great Northern Highway, providing excellent regional access and strong infrastructure support for future development. Koongie Park/Halls Creek benefits from existing granted Mining Licences, significantly reducing the regulatory pathway and lead time to development.

Polymetallic Deposit

The project is anchored by two significant base metal deposits, Sandiego and Onedin, hosted within the Proterozoic Koongie Park Formation, a recognised volcanic-massive-sulphide environment known for copper, zinc, lead and silver mineralisation. Extensive historical exploration, including over 300 reverse circulation (RC) and diamond drill holes totalling more than 60,000 metres, confirms the presence of substantial polymetallic mineralisation at the project.

The combined Mineral Resource Estimates at Sandiego and Onedin include 89,000 of tonnes of copper, 69,000 tonnes of lead, 326,000 tonnes of zinc plus 9.2 million ounces of silver. Historical work demonstrates the project’s potential as a multi-commodity base metal system with both near-term development and long-term growth potential.

Attractive Economic Potential

Cobalt Blue’s June 2025 Scoping Study for the Halls Creek Project highlights a multi-stage development pathway designed to generate early cash flow and unlock the project’s inherent value. The study outlines an initial 10.5-year mine life, split between open-pit mining at Onedin and underground operations at Sandiego. The study indicates robust economic metrics, including estimated net present value and internal rates of return that support the case for further technical evaluation and potential development.

The 2025 Scoping Study revealed:

- 10.5 year project life

- Pre-tax NPV 8% (real) of A$172m

- Pre-tax Internal Rate of Return of 28%

- Start-up Capex of A$73m

- Payback period of 3.5 years

| Commodity | 2025 Scoping Study Price | Current Price (Spot) | Price Increase |

|---|---|---|---|

| Copper | $10,002 (US$/t) | $12,980 (US$/t) | +29.5% |

| Zinc | $2,780 (US$/t) | $3,325 (US$/t) | +19.6% |

| Silver | $26.48 (US$/oz) | $83.71 (US$/oz) | +216.1% |

The 2025 Koongie Park/Halls Creek Scoping Study was completed using conservative commodity price assumptions that reflected long-term consensus forecasts at the time. Since then, market conditions have shifted materially, with copper, zinc and silver prices trading well above the levels used in the study.

Applying current prices results in a significant increase in gross metal revenue, driven primarily by higher copper and zinc prices and a substantial uplift in silver pricing. In particular, silver prices are now more than three times higher than those assumed in the Scoping Study, materially enhancing by-product credits and overall project margins.

On an indicative basis, the uplift in pricing supports a materially higher net present value, an improved internal rate of return and a shorter capital payback period.

NPV (A$M): increases from ~A$172M to ~A$255M

IRR: improves from ~28% to ~35%

Payback: shortens from ~3.5 years to ~2.5 years

Conclusion

AuKing Mining has assembled a portfolio of projects that combines historical discovery success, strong geological fundamentals and exposure to buoyant commodities.

In Tasmania, the Big Wilson tin discovery stands out as a compelling example of under-explored potential in a proven mineral province. The standout discovery hole delivered 35.4 metres at 1% tin (Sn) yet the prospect has not been systematically followed up since the original drilling campaign.

Located within a region that hosts the Renison operation and other significant tin deposits, the surrounding tenements are considered highly prospective for additional greisen and vein-style tin systems. With global tin supply constrained and limited new discoveries being made, Tasmania presents an opportunity to unlock value in a tier-one jurisdiction with established infrastructure and processing capabilities.

In Tanzania, the Mkuju River project positions AuKing within one of Africa’s recognised uranium districts. The broader region hosts large, defined uranium deposits and established resource inventory, highlighting the scale of mineralisation within the basin. Early exploration work has confirmed the presence of uranium and geochemical signatures consistent with nearby deposits, providing a solid technical foundation for further exploration. With uranium markets strengthening on the back of global nuclear policy support and energy security initiatives, the project offers exposure to robust uranium prices.

In Western Australia, the Koongie Park or Halls Creek project consists of a substantial polymetallic copper-zinc-silver system in the Kimberley region. The 2025 Scoping Study demonstrated strong base case economics, and when considered against current commodity prices, the project shows materially enhanced value potential. Importantly, Koongie Park benefits from an existing granted Mining Licence, supporting a streamlined pathway to development. The project’s scale, grade profile and commodity mix provide strong leverage to tightening copper and zinc markets and elevated silver prices.

Collectively, these assets provide diversification across tin, uranium and base metals, all commodities with strong structural demand drivers in 2026. With supportive macro fundamentals, exposure to constrained supply environments and assets located in established mining jurisdictions, AuKing Mining is well positioned to generate shareholder value as these projects are progressed.

The company also boasts substantial shareholders with a proven track-record.

As at 22 January 2026, Gage Resources held 60,000,000 shares in AuKing Mining, representing 5.14% of the company. On the same date, Asimwe Kabunga held 82,080,000 shares, representing 7.03% of AuKing Mining.

Gage Resources is a subsidiary of Beijing Gage Capital Management, a Beijing-based private equity group with more than US$1.6 billion in funds under management. The group has demonstrated a strong track record in ASX investments, most notably through its involvement in Larvotto Resources (ASX: LRV). Gage subscribed for 41,180,792 placement shares for approximately $2.8 million, equating to 6.8 cents per share and representing 19.9% of the company at the time. Since that investment, Larvotto’s share price has reached a high of $1.67 per share, representing a gain of approximately 2,356% from Gage’s entry price.

Asimwe Kabunga played a pivotal role in the growth of Lindian Resources (ASX: LIN), where he served as founder and chairman. Under his leadership, Lindian acquired and advanced the Kangankunde Rare Earths Project, positioning it as a globally significant rare earths asset. Kabunga was also a substantial shareholder in the company. During this period, Lindian Resources attained a market capitalisation in excess of A$700 million.